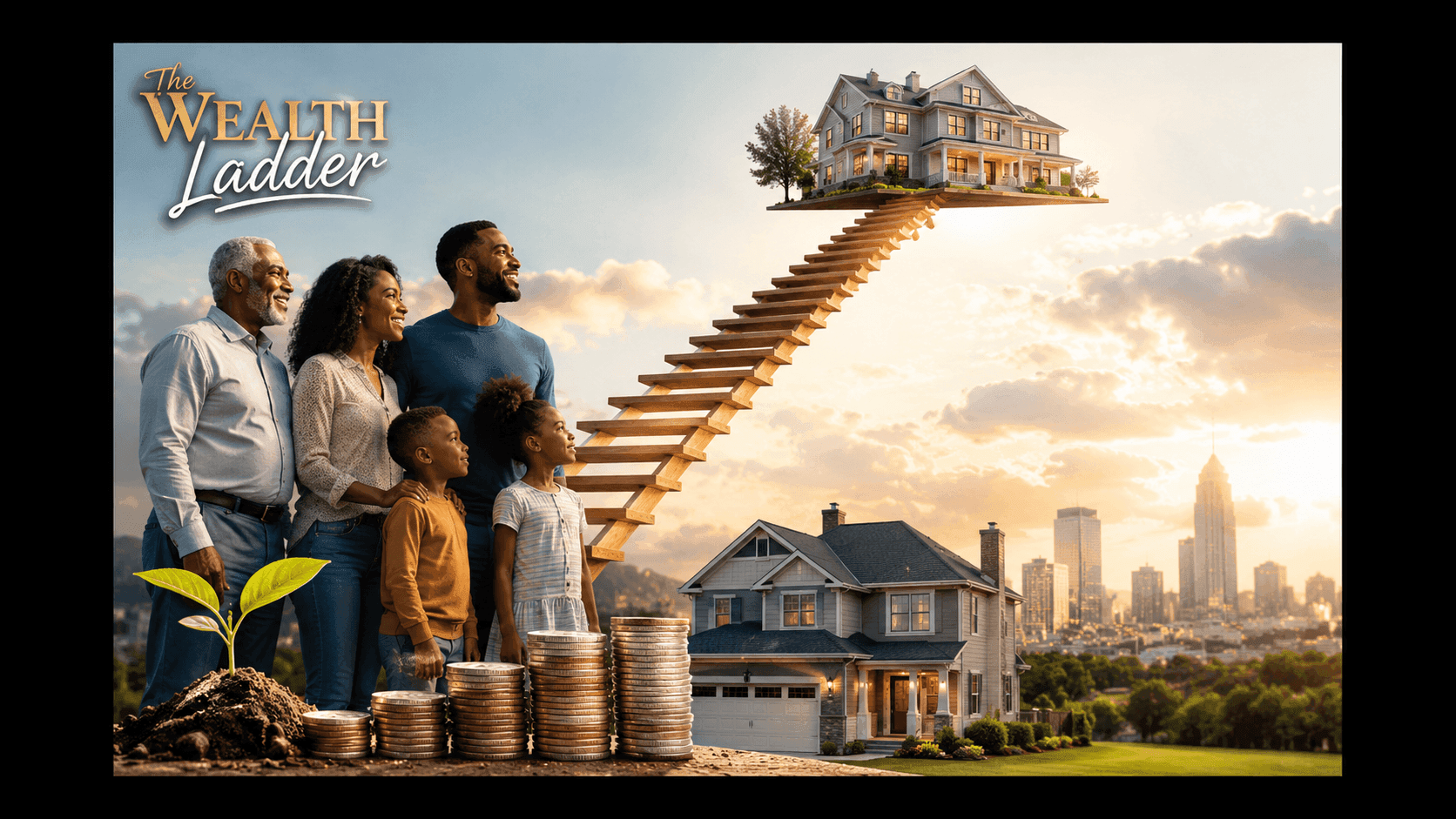

The Wealth Ladder

When people think about building wealth, they often focus on investments, retirement accounts, or growing a business. While those can all play an important role, one of the most common ways families have built long term financial stability is through homeownership.

First, each mortgage payment may reduce the amount owed on the loan. Over time, this can increase a homeowner's equity, which is the portion of the property they truly own.

Second, homes may appreciate in value over the years. While appreciation is never guaranteed, many homeowners have benefited from rising property values over extended periods of time.

Together, these two factors can work like a ladder, with each step potentially moving a family closer to greater financial flexibility and long term security.

How Homeownership Can Build Wealth

Some of the potential financial benefits include:

• Building equity through mortgage payments

• Creating a financial asset that may be leveraged for future goals

• Providing greater housing stability compared to renting

• Building generational wealth

One of the biggest misconceptions about real estate is that successful homeowners perfectly timed the market. In reality, many families who accumulated wealth through homeownership did not buy at the absolute lowest point or sell at the highest point. Instead, they focused on purchasing a home they could comfortably afford and then allowed time to work in their favor. Over the years, consistent mortgage payments combined with potential property appreciation often helped create significant equity. That equity became a resource that could support important life milestones and opportunities.

The Long Term Impact

For many homeowners, accumulated equity has helped fund:

• College education expenses for children

• Retirement planning and financial security

• Home improvements and renovations

• The purchase of a larger or more suitable home

• Business ventures or other investments

• Financial support for future generations

A home is more than just a place to sleep, eat, and spend time with family. For many people, it becomes one of their largest financial assets and an important part of their overall wealth building strategy. The key lesson is that wealth often grows gradually rather than overnight.

In that sense, homeownership can be viewed as a wealth ladder, where each step may bring a family closer to achieving future goals, creating financial flexibility, and building a stronger foundation for generations to come.

Disclaimer: Real estate values can rise or fall and are not guaranteed. This article is for educational purposes only and should not be considered financial, tax, or legal advice. Consult qualified professionals regarding your specific situation.